Credit tips for buying a home

We all should know that it’s important to have solid good credit when thinking about buying your first home. We all know that lenders and banks want to see solid credit in any borrower.

But what exactly does that mean for first time home buyers?

It means having some credit. It means having a score in the mid-to-upper 600 range (although that doesn’t mean you’re out in the cold if you’re in the low 600’s). It means no major negative items like a repo or bankruptcy in the past few years.

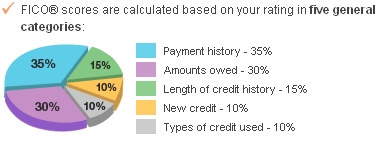

In short, it means you’re responsible with your money, and you pay your bills on time. The way lender determine if you are doing these things is with a FICO credit score.

How do you make sure your credit is good in general? Let’s explore 6 credit tips for first time home buyers that you could follow even if you’re not a first time buyer.

- Pay your bills on time, every time. This is a simple rule when it comes to establishing good credit (not always easy to follow, but it’s vital). You have to keep your bills current.

- Have a diverse credit portfolio. This can include secured credit cards, a small car loan and maybe a store credit line. A diverse mix shows that you are able and willing to pay your bills.

- Keep your credit charges below 30% of the limits. Going above this number will reduce your credit score. Paying the debt down is the best way to make this happen. You could also ask the credit company to raise your limit (but don’t charge more if they do!).

- Check your credit history every quarter. You have a right to know what’s on your credit report. Thanks to the government, you actually have the legal right to get your credit report once a year from each of the 3 credit bureaus. That means you can actually check your credit report 3 times per year.

- Keep your lines of credit open. Closing a paid-off account is a good step after you have your mortgage. A longer, more diverse credit history is important.

- Once you have a few lines of credit, don’t open any more. Continuously opening new credit accounts is risky, and your score will reflect this.

You can explore more on how to get your credit ready to become a first time home buyer with reading “The Understanding Your FICO Score” at the button below. The Pamphlet covers what makes up a credit score, how to improve your FICO score, steps to rebuilding credit and more.