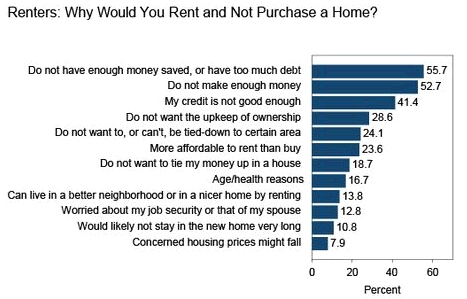

Closing Costs on a Home Mortgage

All home mortgage loans have fees knows as closing costs, which are required to process and obtain your home loan.

People involved include the lender, title companies, appraisers, credit bureau, county document recording fees, and even state mortgage deed taxes.

You also need to buy you first years home owners insurance, and pay pro-rated property taxes based on when taxes are due, how much they are, and what month you buy the home.

All of these closing costs can really add up, and are in ADDITION to your down payment. Your Loan Officer can give you a breakdown of what all these costs will add up to when you apply for your home loan.

There are 4 basic ways to pay your loans closing costs:

- Pay cash out-of-pocket at closing

- Get a downpayment and closing cost assistance loan

- Roll the closing costs into the loan amount – This is commonly known as “Seller Paid Closing Costs”

- Roll the closing costs into your loan by taking a slightly higher interest rate (not available on all loans)

or a combination of any or all of these options

NOTE: All lenders have basically the same closing costs. Any lender quoting closing costs significantly less than anyone else is just doing option 4, but not telling you.

NOTE: All lenders have basically the same closing costs. Any lender quoting closing costs significantly less than anyone else is just doing option 4, but not telling you.

Paying your loans closing costs out-of-pocket is always best in the long-term, but simply not realistic for most first time home buyers. Between all the other options to pay closing costs, most people are able to buy a home with ONLY needing their down payment.

CLOSING COSTS AND FEES NEEDED UP FRONT

Some fees and closing costs are required up-front by your mortgage company when buying a home. The two most common items are:

Paying for a credit report at time of application. This runs between $10.00 to $20.00

Paying for the appraisal once your offer to buy a home is accepted. This runs between $375 to $500

COSTS REQUIRED TO BUY THE HOUSE

Of cost there is your down payment. Your Loan Officer will discuss how much you will need after reviewing your full loan application, and determining what mortgage program you qualify for, how much the house is you are buying, and if you are using any downpayment assistance programs.

There are two up-front costs many people don’t understand you need when buying a home.

The first is earnest money. This is required by the seller as good faith money when you make your offer to buy.

It can vary, so talk to your Real Estate Agent, but at least $1,000 is very common in Minnesota. The earnest money gets credited towards your down payment and closing costs.

The idea is if your offer is accepted, but then later you decide not to buy the home, they keep your earnest money for wasting the sellers time. So be sure you are serious when making an offer to buy a home.

The second is a Home Inspection. After your offer to buy the home is accepted, it is very common, and very smart to get an inspection on the home to make sure there are no hidden surprises. Talk to your Real Estate Agent to set up a home inspection. Home inspections generally run around $300 – $400.

THE INITIAL FEES WORKSHEET AND GOOD FAITH ESTIMATE

Talk to your Loan Officer about getting a full breakdown of how much money you will need out-of-pocket to buy your new home.

This detailed breakdown will show you everything you need to know, and the final amount of money needed at the actual closing.

It is show your down payment, and all your closing costs. Then it will show you any credits to these costs, including seller paid closing costs, lender credits for interest rate, and any items you have already paid, like credit reports, appraisal, and earnest money.

Before you have the exact house, you will get an initial fees worksheet – or a close estimate based on the ballpark price of the homes you are looking at.

Once you actually buy a house, and we know the exact address, exact purchase price, etc., you will receive a Good Faith Estimate, which while still an estimate, will be incredibly close to the exact penny you will need to finalize your home purchase.

As always, feel free to contact our first time home buyer expert Loan officers at (651) 552-3681 with ANY question whatsoever. We lend in MN, WI, IA, ND, SD only. For more accurate service, complete the online loan application first.