Tips to Improve Your Mortgage Approval and Credit Score

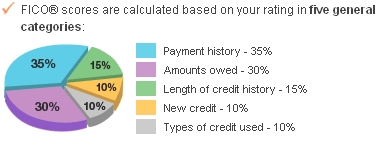

When you are looking to purchase a home, or refinance your exiting home, your credit score is very important. One of the first things your lender will do is check your credit report to assess your creditworthiness.

As everyone knows, the better your credit score, the more options you have, and the lower the mortgage interest rates will be available to you.

However, if you have a very bad credit score, it could be causing you to be offered high interest rates on your mortgage that could cost you thousands more in higher payments over the years, and worse yet, cause you to be denied.

Improving your credit score before getting a mortgage loan will ensure that you get the best interest rate possible.

But what can you do to improve your credit score?

Here are a few tips that can help you improve your credit score:

Be Patient – Fixing Credit Takes Time

A good analogy for improving credit is a little bit like losing weight. You might see a big jump right away, then getting to your full goal may take awhile. But the long term benefit of your new good habits that will make all the difference in the future

When it comes to all of the ways to improve your credit score, there can sometimes be something you can do quickly, and other take a long time. Just like weight loss, there are no magic quick-fixes. The best way to rebuild your credit is to be responsible over time.

Check Your Credit Report For Errors

Your first step is to review your credit report. Your loan officer is a good place to start, or you can get a copy from www.CreditKarma.com or www.AnnualCreditReport.com. Check it over carefully for errors, and contact the original creditor to correct those errors.

Pay Down debt

Credit cards cause a lot of score damage. This is primarily because the scoring model looks at your credit limit, and then how much you have currently on the card. Think of it in terms of 1/4 percent. If you have less than 25% of the limit used, this is considered good utilization of credit. If you are over 75%, or worse yet, max’ed out, you are killing your credit score.

Set Up Payment Reminders

Late payments spread all over your report can be one of the biggest negative factors bringing down your score. If you have issues paying in a timely manor, simply set up automatic payments, and set up alerts on your accounts to be notified by email or a text whenever your payments are due.

Major Derogatory Items, like Bankruptcy and Foreclosure

Needless to say, these items serious hurt your credit score. The most important thing to do to restore your credit is to get or maintain current and active credit. You see, the scoring model will see the old nasty negative items. But they want to see how you are TODAY. Have you gotten back on track? If you don’t have current credit, your score will never recover.