St Paul, MN: Virtually, all homeowners have lost value on their homes in recent years. For many, this has created some challenges to refinancing and taking advantage of today’s super low mortgage interest rates.

There are a few programs with can help, depending on what type of mortgage loan you have today. May people have successfully used program like HARP (Home Affordable Refinance Program), the FHA Streamline Refinance, or even the VA Streamline refinance known as an IRRRL loan.

Sadly, not everyone fits the criteria. Therefore Washington has been floating the idea of an expanded HARP 3 Refinance Program. It doesn’t exist yet, and may never exist… But if it does, here is what it may look like:

Current loan is NOT backed by FHA, USDA, Fannie Mae, Freddie Mac

Primary home only. No second homes or investment home

Loan less than $750,000.

On time mortgage payments for the past 6 months, with no more than one 30-day late payment in the past year.

Credit score above 580

This new HARP 3 refinance program proposal mirrors the current HARP 2.0 refinance loan program (possible no appraisal, less document, etc), except it would potentially also allow any underwater home owner, not just those who have a loan owned by Fannie Mae or Freddie Mac.

Try out the governments “Would I qualify for a refinance” below..

Minneapolis, MN: Home mortgage loans defaulted at a higher rate in the last quarter of 2012. This is unwelcome news compared to an overall trend of good news in the housing and real estate market

Homeowners defaulting on the home mortgage loans has increased for three consecutive months after hitting a post-recession low in September, according to a recent report. Mortgage defaults averaged1.36 percent of all loans in September 2012. Since then, defaults on home mortgages rose to 1.47 percent in October, 1.58 percent in November and 1.68 percent in December.

Experts are confused as to why this is happening, as the general housing market has been improving. Foreclosures have been on the decline. New homes sales are up, and with the continuance of historically low mortgage interest rates, first-time home buyers have been snapping up low priced real estate for some time now.

2012 showed a nice improvement in the quality of consumers loans, like cars and credit cards, but first and second mortgage loan defaults have been holding the overall default rate up.

Minneapolis, MN: Freddie Mac yesterday released the results of its Primary Mortgage Market Survey® (PMMS®), showing fixed mortgage rates moving higher following December’s employment report. The 30-year fixed averaged 3.40 percent, its highest reading in eight weeks. The all-time record low for the average 30-year fixed was 3.31 percent set November 21, 2012.

News Facts

30-year fixed mortgage rates (FRM) averaged 3.40 percent with an average 0.7 point for the week ending January 10, 2013, up from last week when it averaged 3.34 percent. Last year at this time, the 30-year FRM averaged 3.89 percent.

15-year fixed mortgage rates this week averaged 2.66 percent with an average 0.7 point, up from last week when it averaged 2.64 percent. A year ago at this time, the 15-year FRM averaged 3.16 percent.

5-year adjustable mortgage rates (ARM) averaged 2.67 percent this week with an average 0.6 point, down from last week when it averaged 2.71 percent. A year ago, the 5-year ARM averaged 2.82 percent.

Quotes Attributed to Frank Nothaft, vice president and chief economist, Freddie Mac.

“Fixed mortgage rates increased slightly following a positive employment report for December. The economy added 155,000 jobs, above the consensus market forecast, and November’s job growth was revised upward by another 24,000 workers. This helped keep the unemployment rate steady at 7.8 percent, the lowest since December 2008. For all of 2012, 1.86 million jobs were created and represented the largest annual gain since 2006.”

Freddie Mac’s survey is the average of loans bought from lenders * last week, including discount points. Applicants must pay all closing costs at these rates. No cost loan rates higher.

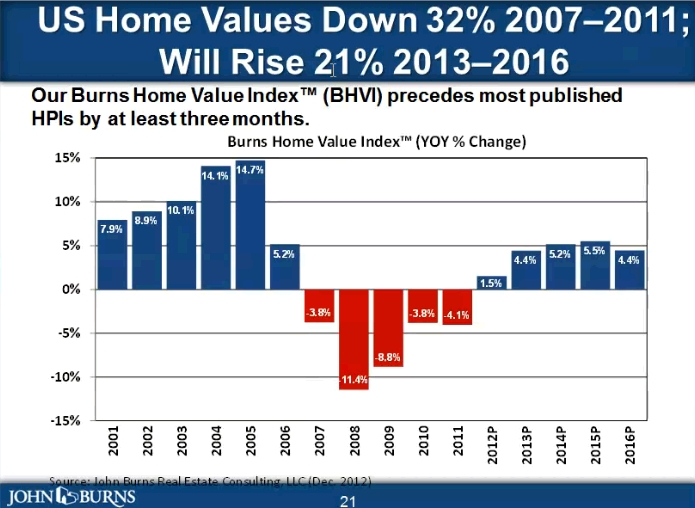

Minneapolis, MN: Homes values have certainly seen a roller-coaster ride. The big run up in from 2000 to 2006, then the crash.

The big question in everyones mind, is what will happen to values in the future? Looking at the chart below, you can see an anticipated rise of 21% in values by 2016.

This is great news all around. Those with existing homes who have lost value should regain a lot. Those buying at today’s rock bottom home prices, and rock bottom low interest rates should see nice appreciation.

What clients and Real Estate Agents Don’t Understand About Appraiser Independence

Minneapolis, MN: Real Estate Agents constantly call our mortgage office to ask if an Appraisal was ordered, or if it is completed yet.

The first question is pretty silly… Of course it was. The second question is tougher to answer until the completed appraisal physically shows up on the lenders desk.

Recent lender rules require what is known as “Appraiser Independence”. This is a double down on the old rules that no one is allowed to influence or pressure the appraiser to obtain any pre-determined value on the home. The rules also means that no one who will be compensated on the file can have anything to do with picking the appraiser. It has to be totally blind and randomly assigned. This is very different from years past where the client or the Loan Officer could pick any appraiser they wanted.

Once the appraisal has been ordered, there are varying degrees of what the Loan Officer may or may not know about the status of the appraisal. Most mortgage companies use a middle company, known as an AMC, or Appraisal Management Company, to handle all aspects of the appraisal. This easily means the lender will meet the “independence” guidelines. Some AMC’s are better than others in letting the lender know the status, giving them the expected date the appraiser will visit the property, and the expected appraisal completion date. With many others, the lender is completely in the blind. In the vast majority of cases, I don’t even know who the appraiser is until the appraisal is completed.

To further complicate the issue, while it is technically possible for a Loan Officer to speak to an appraiser on a very limited number of questions, the vast majority of lenders completely forbid this contact to avoid even the remote likelihood of influence complicity. It is much easier to respond to regulators that “our loan officers are forbidden”, then to claim they didn’t do anything wrong.

As a mortgage lender, it is very frustrating when real estate agents constantly bombard me with appraisal question. If I know, I will tell you. Do not yell at the Loan Officer if they don’t know the answer or say they can not talk to the appraiser.

Successful house hunting starts with mortgage pre-approval – Not talking to a Real Estate Agent.

What Is Mortgage Pre-Approval

Minneapolis, MN: Mortgage pre-approval is what happens when you talk to a Loan Officer and find out how much house you can afford. It’s an important step because it helps your real estate agent zero in like a laser beam on the correct house price for you. Your mortgage consultant will ask questions about your financial situation, including job, income, assets, debts, and more. Then you’ll talk to them about your comfort level when it comes to a monthly mortgage payment. It’s important to know this, in order to avoid buying a home you really can’t afford.

FHA Mortgage Loan Expert in MN and WI

At this point, you are NOT pre-approved.The next step to full pre-approval is submitting all your documents to the lender. Common items include; photo ID, pay stubs, W2’s, and bank statements. Once the mortgage company reviews these documents, THEN you will be pre-approved!

Here’s a look at some of the benefits to getting pre-approved before you house hunt:

Powerful Buyer. Sellers often give preferential treatment to pre-approved buyers since they know for sure that you can finance the purchase. If you get into a bidding war with another buyer, the seller might look at your offer in a better light than someone who hasn’t talked to a mortgage consultant.

Interest Rates. As interest rates go up and down, you can get in on a locked rate before they go up again. You can lock in an interest rate if you are pre-approved, as soon as you have a signed purchase contract. A lower interest rate will save a lot of money over the life of that mortgage.

Credit Surprises.Mortgage pre-approval reduces credit surprises. If you wait until the last minute to secure financing and find that you have a few issues that need to be resolved with your credit, you could miss an opportunity to purchase your dream home. Getting pre-approved will help you head-off surprises so you can go look for the perfect home.

Mortgage pre-approval is as close as anyone can get to insuring you’ll be able to obtain a mortgage loan in advance of finding a home. Pre-approval gives MN and WIfirst time home buyers a definite idea of what they can afford and shows sellers that they are dealing with a serious buyer.

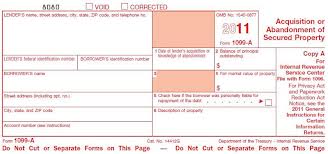

Minneapolis, MN: When debt is relieved or written off… That “relief” is supposed to be taxed as income. The lender gives the debtor a Form 1009-C, Cancellation of Debt if the cancellation equals $600 or more. When it comes to a foreclosure or abandonment of secured property, it is a form 1099-A.

That means if someone owes $150,000 on their home and it sells for $100,000 in a foreclosure auction, they could owe taxes on the remaining $50,000. For someone in the 25% tax bracket, that would mean paying $12,500 in taxes on the foreclosure. Similar taxes would apply for amounts that were forgiven in short sales and principal reductions.

The Mortgage Forgiveness Debt Relief Act of 2007 basically said that mortgage lenders were not to give the 1099 for foreclosures, saving those who have already lost a home significantly on their taxes.

The Mortgage Forgiveness Debt Relief Act was set to expire Dec 31, 2012., and that scared a lot of people. Fortunately, Congress wisely EXTENDED the Act as part of the Fiscal Cliff Negotiations for at least another year.

The clowns in Washington usually mess things up… But they got this one right!

Minneapolis, MN: Sometimes life happens. Good people end up with bad credit. But for most, bad credit is fixable with a little time, effort, and knowledge. Credit decisions for just about anything, car loans, credit cards, home mortgage loans all depend on your credit score. We all know having a higher score means not only getting the credit, but at lower interest rates.

The biggest item people need to understand is that a huge portion of their credit score is based recent information versus old information. A 30-day late payment on a car loan from 5-years ago DOES show up on your credit report, but it has little impact compared to a 30-day late payment from last month.

Paying off old collections:

There really isn’t much you can do about late payments on your credit report, so an area that many people attempt to correct is any old unpaid collection accounts. In theory, paying off old collection accounts seems like a good way to improve your credit score. but mistakes that lower your score, especially temporarily are most often made here when attempting to improve your credit score.

Date of Last Activity:

Assume you have a 5-year old collection account. It is just two-years from falling off your credit report, and while collections are bad, because of its age, it is only having a small impact on your overall score. By paying it today, you move the date of last activity to a current date. Your credit report now “sees” this payment activity as current. You now have a “current” paid collection, versus an old unpaid collection. While moving a collection from unpaid to paid will help in the long run, it may hurt your score today.

Assume one the other hand you have a one-year old collection account. This is having a major effect on your credit score, and should be taken care of immediately.

Because of how the date of last activity algorithm works, when attempting to improve your credit score, always deal with the most recent negative accounts first.

In the long run, paying off old collection accounts is ALWAYS the best thing to do – but be aware that if you are looking to improve score for a purchase in the short-term, paying off old collection just might end up lowering your score before you see the long-term improvements you desire.

Minneapolis, MN: As mortgage interest rates drop, many people believe that no cost loans, and refinancing multiples times is a game winning strategy. People who do this are known as “serial refinancers.”

A Wall Street Journal report shows about 2.2 million people have refinance their current home loan at least twice since 2009.

All loans have closing costs, so an important aspect to refinancing is the question, “is their a benefit?” Refinancing generally is down to obtain a lower mortgage interest rate, and hence, a lower mortgage payment. Some people also lower their term, going from maybe a 30-year loan to a 20-year, 15-year, or even a 10-year.

How do you pay closing costs?

There are a few ways to pay loan closing costs: Cash, roll into new loan amount, hide in interest rate, or a combination of any of these options. The most common way is rolling into a higher new loan amount, but a loan of people roll at least some, if not all into the interest rate. This achieves a low cost, or no closing cost refinance.

If done smartly, a serial refinancier can dramatically improve their situation and reduce the long-term cost of their home loans. If done wrong, while you may be lowering your payment today, you never get anywhere as you constantly reset your loan back to a 30-years.

Many people believe you must meet a certain percentage before you should refinance. A common number I hear is 2% lower. I couldn’t disagree more! The formula is simple, and could be significantly less of a percentage. Simply divide the savings by the cost. If you are likely to be in the home significantly longer than the breakeven period, it probably makes sense to refinance.

So is it worth refinancing?

You have everything to gain and nothing to lose to see significant savings in your mortgage payment with today’s historic low rates? Contact a local NON-Bank licensed loan officer – give them a full mortgage application, and let them crunch your numbers. If may be well worth refinancing again, even if you just did it a short time ago.

As a side note… Contrary to popular belief. In most cases, the WORST place to refinance is with your CURRENT Lender. Feel free to talk to them, but get a second opinion!

ST Paul, MN: Freddie Mac today released the results of its Primary Mortgage Market Survey® (PMMS®), showing fixed mortgage rates mixed following data reports on inflation and the housing construction market. The 30-year fixed moved up averaging 3.37 percent, while the 15-year fixed eased to 2.65 percent, both remaining near their record lows.

News Facts

30-year fixed-rate mortgages (FRM) averaged 3.37 percent with an average 0.7 point for the week ending December 20, 2012, up from last week when it averaged 3.32 percent. Last year at this time, the 30-year FRM averaged 3.91 percent.

15-year fixed rate mortgages this week averaged 2.65 percent with an average 0.7 point, down from last week when it averaged 2.66 percent.A year ago at this time, the 15-year FRM averaged 3.21 percent.

5-year adjustable (ARM) mortgages averaged 2.71 percent this week with an average 0.7 point, up from last week when it averaged 2.70 percent. A year ago, the 5-year ARM averaged 2.85 percent.

Quotes Attributed to Frank Nothaft, vice president and chief economist, Freddie Mac.

“Mortgage rates were mixed this week following data reports on stable inflation and a thriving home construction market. The 12-month growth in the core consumer price index has remained between 1.9 and 2.1 percent for the past five consecutive months ending in November. Meanwhile, housing starts averaged the strongest three months in November since September 2008, and homebuilder confidence rose in December to its highest reading since April 2008.”

Freddie Mac’s survey is the average of loans bought from lenders * last week, including discount points. Applicants must pay all closing costs at these rates. No cost loan rates higher.

Everyone hates paying for insurance… but be it car insurance, health insurance, home owners insurance, life insurance, or renters insurance. You are sure happy you have it when you need it.

Renters tend to be younger and make less money than homeowners, and they don’t always think about the need for renters insurance.

Get a FREE Rental Insurance Quote

Many people focus simply on their contents, thinking they don’t have that much stuff. If all this stuff disappeared tomorrow, they could easily replace it. But there’s more to renters insurance than protecting your belongings. Here’s what you should think about when you consider a renters policy.

Fire, smoke, and water damage are usually the other events that we think of when we talk about renter’s insurance. But be sure to ask your agent what is and is not included in your coverage. It is important to note that the tenant is NEVER covered under the property owner’s policy.

What does Renter’s Insurance Cover?

You will be protected if your apartment burns down, or the upstairs tenants water heater leaks and drains into you unit, or if you are robbed of those expensive gadgets that you possess. Many policies cover medical expenses if someone is hurt inside your property and liability insurance can help protect your assets too. If the loss forces you to move out of the unit, the coverage includes increased living expenses. If you live in a flood plain, flooding will not be covered.

How much coverage do I need?

This will be determined by the value of the things that you have. If you have a lot of expensive things, (jewelry, electronics, furnishing) you can expect to have a larger policy. The cost will vary in proportion to the coverage. Be sure to ask about the limitation of the policy. Many policies limit the amount of coverage on electronics and assets used for working at home may require separate coverage.

What does Renter’s Insurance cost?

On average, most people spend about $150 a year, depending on the amount covered, and where you live. If you have expensive things, your costs will be higher. High risk areas can boost the premium as well. If you are considering whether or not to get insurance, remember that a fire caused by a smoker who falls asleep with a burning cigarette next door could cost you everything but the cloths on your back.

Three underserved groups – Are you one of these?

There are three groups that seem to be lacking insurance coverage.

College student – Fresh off to school, not really thinking about losing their belongings, college students are finding that theft, vandalism, and fire can quickly take away their possessions.

Elderly – This group may have been long time home owners but the loss of a loved one has forced them to rent a more affordable home or apartment. The idea of renter’s insurance is being overlooked.

Those transitioning from foreclosure to rental – This group are rather large; many have lost their home to foreclosure and are now renting for the first time in a long time. As homeowners, they probably had homeowners insurance but just haven’t considered getting renter’s insurance.

If you are a renter, consider finding a rental insurance agent near you. The cost really isn’t all that great, and will protect you in the event of a loss. Be sure to ask a lot of questions about the policy; what is included, exceptions and exclusions, and cost all need to be talk about before signing the agreement.

Mortgage Rates Ease Slightly, Remain Near Record Lows

Minneapolis, MN: Freddie Mac today released the results of its Primary Mortgage Market Survey® (PMMS®), showing fixed mortgage rates easing slightly and remaining near record lows to keep homebuyer affordability high and attractive to those looking to refinance.

News Facts

30-year fixed-rate mortgages (FRM) averaged 3.32 percent with an average 0.7 point for the week ending December 13, 2012, down from last week when it averaged 3.34 percent. Last year at this time, the 30-year FRM averaged 3.94 percent.

15-year fixed rate mortgages this week averaged 2.66 percent with an average 0.6 point, down from last week when it averaged 2.67 percent.A year ago at this time, the 15-year FRM averaged 3.21 percent.

5-year adjustable rate mortgages (ARM) averaged 2.70 percent this week with an average 0.6 point, up from last week when it averaged 2.69 percent. A year ago, the 5-year ARM averaged 2.86 percent.

Quotes Attributed to Frank Nothaft, vice president and chief economist, Freddie Mac.

“Mortgage rates held relatively steady following the November employment report. Although 146,000 jobs were created, above the market consensus forecast of 85,000, revisions subtracted 49,000 workers over the September and October period. The unemployment rate fell from 7.9 to 7.7 percent. However, in its December 12 monetary policy statement, the Federal Reserve (Fed) noted that this rate remains elevated and modified the statement to tie any increases to its target rate to the unemployment rate falling below 6.5 percent. The latest Fed central-tendency forecast is for unemployment to be between 7.4 and 7.7 percent in the fourth quarter of 2013 and between 6.8 and 7.3 percent by late 2014.”

Freddie Mac’s survey is the average of loans bought from lenders * last week, including discount points. Applicants must pay all closing costs at these rates. No cost loan rates higher.

Have a small side business? Disclose it to your Loan Officer

St Paul, MN: It is a pretty well know that when buying a home and applying for a home mortgage loan these days, mortgage companies are asking for more information from the applicants.

Standard items include photo ID, last 30-days of pay stubs, last two years W2’s, and your last two months of bank statements. What is less known are some of the additional requirements that can quickly derail your pre-approval.

When taking your application, your Mortgage Loan Officer will ask details about your employment. If your job is paid hourly or salary, the lender does NOT need a copy of your Federal Tax Returns, so of course they would not ask you to provide them.

If you are self-employed, get tips, or commission income – your last two years of tax returns ARE required, so the Loan Officer will ask you to provide them right away.

But what if you have a small side business? It is likely you didn’t mention it. How about the spouse? Do they have a small side business. Mary Kay, Tupperware, or maybe Lia Sofia?

The 4506T: All mortgage applications now require the applicant to sign an IRS 4506T. This document allows the mortgage lender to obtain a copy of your Federal Tax Returns.

They are looking for any discrepancies between what you told the lender and what you reported to the IRS.

Deal Killers: I recently Pre-Approved a couple. Only the husband and his salary job were listed on the application, but the loan was denied a week before closing when we discovered the wife reported a $15,000 loss on their joint tax return for her jewelry business.

Any side business losses will by underwriting be assumed to continue. Therefore in this case, I was forced to reduce the husbands income by $15,000 a year, which caused them to exceed debt-to-income ratios and have thier mortgage loan application denied.

This particular couple lost the dream house they were trying to buy. In the end, they were able to buy and close on a slightly less expensive home, based on their actual situation. Had this business loss been known in the beginning, they could have focused their home search on the correctly priced home, and saved a lot of time and headache.

The Bottom Line: If it is on your tax return, the lender is going to know it . Disclosed everything up front to your Loan Officer, no matter how trivial it may sound to you.

Minneapolis, MN: Recent reports show homes builders are making record profits – but not from building homes! What then you ask? From providing the mortgage loans the “builder” give to people buying their homes!

Pulte Homes shows mortgage loan revenue up 70%, which is 6 times higher than their revenue from building homes. Home builder Lennar Homes shows mortgage revenue up 60%!

The reason? The margins on the loans they force… Oops… Offer people buying their homes are fat. Really fat.

It is a well known fact that home buyers can get significantly better mortgage loans deals when NOT using the builders in house lender, but home buyers don’t seem to care because they are blindsided by the shinny new object (the home), and fall for the tall tails the builder throw at them – items like “no closing costs”, and “appliance allowance” that are already being paid for within the cost of the home itself. It is no “deal”.

Most new construction home buyers fail to ask, or even realize how the builder is able to give them these freebees… and that in most cases, you could still get those items AND get a better mortgage loan with someone else, if the buyers just had a little better negotiation skills and employed a “buyer agent” real estate agent instead of simply working with the builders agent.

Many people think the days of sleezy tactics, high pressure sales, and low balling customers on interest rates and closing costs are gone because of new regulation – and they are for the most part, unless you are working with a new construction builder, in which case, the government seems to be looking the other way.

No wonder builders are making a killing in the mortgage loan business!

Minneapolis, MN: I expect long-term 30-year fixed rates to remain +/- about 3.50% for the first 6 months of 2013, with a slow but steady increase the second half of 2013 – but with the 30-year fixed rate remaining under 4.00% the entire year.

I also expect to see property values to slowly rise, with the average home increasing in value about 3% nationwide. While that doesn’t sound like much, it is well within long-term historic appreciation levels.

Homeowners defaulting on the

Homeowners defaulting on the  Minneapolis, MN: Freddie Mac yesterday released the results of its Primary Mortgage Market Survey® (PMMS®), showing fixed mortgage rates moving higher following December’s employment report. The 30-year fixed averaged 3.40 percent, its highest reading in eight weeks. The all-time record low for the average 30-year fixed was 3.31 percent set November 21, 2012.

Minneapolis, MN: Freddie Mac yesterday released the results of its Primary Mortgage Market Survey® (PMMS®), showing fixed mortgage rates moving higher following December’s employment report. The 30-year fixed averaged 3.40 percent, its highest reading in eight weeks. The all-time record low for the average 30-year fixed was 3.31 percent set November 21, 2012.

The first question is pretty silly… Of course it was. The second question is tougher to answer until the completed appraisal physically shows up on the lenders desk.

The first question is pretty silly… Of course it was. The second question is tougher to answer until the completed appraisal physically shows up on the lenders desk.

The biggest item people need to understand is that a huge portion of their credit score is based recent information versus old information. A 30-day late payment on a car loan from 5-years ago DOES show up on your credit report, but it has little impact compared to a 30-day late payment from last month.

The biggest item people need to understand is that a huge portion of their credit score is based recent information versus old information. A 30-day late payment on a car loan from 5-years ago DOES show up on your credit report, but it has little impact compared to a 30-day late payment from last month.